This is Part 2 in a two-part series about LLCs. In Part 1, I covered “Why People Should Create LLCs?”

How should I setup my LLC?

Once you know why you need to create an LLC, there are a number of considerations that go into how to set up your LLC to maximize asset protection. Among the most common questions I get when it comes to setting up an LLC are: (1) Which state should I use to form my LLC? and (2) Who should the owner be of my LLC?

To analyze these two questions, we should have a better understanding of what is meant by the concept that LLCs provide asset protection since many people confuse inside liability with outside liability protections.

The Difference Between Inside and Outside Liability Protections

Most people understand that one of the main reasons for creating an LLC is to protect your personal assets from lawsuits. This is known as inside liability protection. For example, if your rental property is owned by your LLC, then if someone is injured on your property and sues the owner, they will have to sue the LLC – not you personally. In that lawsuit, the most that you can lose is whatever is owned by the LLC. We can say that the LLC provided the owner with inside liability protection, because the liability came from “inside” the LLC (the rental property) and what is excluded from the lawsuit is the LLC owner’s personal assets, which are separate and apart from the LLC.

One lesson to appreciate at this point is that an LLC ideally should not own more than one rental property. For example, if an LLC owns three properties (Whitestone, Blackstone, and Evergreen), and an individual is injured on the Evergreen Property, then the plaintiff suing can obtain not only the Evergreen property, but all the properties and assets that the LLC owns, including Whitestone and Blackstone. However, if the three properties were separated out into separate LLCs, the plaintiff injured at the Evergreen property could only sue the Evergreeen LLC and the Whitestone and Blackstone LLCs (and their underlying properties) would be unaffected by that lawsuit.

Many people believe that an LLC also provides outside liability protection. This needs to be fully understood.

If you are at fault during a car accident and get sued, you are being sued personally. Because the lawsuit has nothing to do with your LLC, we call this kind of liability outside liability. The person enforcing a judgment against you will attempt to seize all the assets you personally own. Thus, if you own 50% interest in an LLC, the creditor can attempt to seize your ownership in that LLC. The LLC itself does not protect you from the lawsuit per se, but depending on how the LLC is structured, the result can vary.

While LLCs do a good job protecting from inside liability, the question remains: is there something you can do to protect from outside liability?

The answer is “yes.”

Irrevocable Trusts

Perhaps the greatest tool in the toolbelt of estate planning lawyers is the irrevocable trust. While a full-blown discussion of irrevocable trusts is not the focus of this article, I do make mention of how to use irrevocable trusts in combination with LLCs for maximum asset protection. Thus, it is a good idea to familiarize yourself with the various forms of irrevocable trusts used in estate planning before reading further.

How to Optimize LLCs for Lawsuits

Depending on the state in which you create the LLC and who is the owner of your LLC, you may make it considerably more difficult for a creditor to obtain the assets of the LLC.

1. Which State Should I Use for my LLC?

Many people call our firm after doing Google research. These callers will usually comment, “I’ve read that it’s better to create a Nevada LLC instead of a California LLC, is this true?”

Like any classic legal answer, “It depends.” In short, if you are under the assumption that somehow a Nevada LLC cannot be sued or it automatically protects your assets better than a California LLC, then the answer is, “No, it makes little difference.” If however, you understand the limitations posed even by a Nevada LLC but you still feel that, all things being equal, there is a greater deterrent posed by use of a Nevada LLC, then the answer is, “State law can matter significantly.”

Let’s break this down with an example.

Let’s imagine a client named Cory. Cory owns a California rental property in his name only. Cory recognizes that if he is sued, he stands to lose everything he owns. Thus, Cory is deciding whether to create a California LLC or a Nevada LLC. Which is better for Cory?

But what if we change the nature of the lawsuit against Cory? Instead, what if Cory injures someone in a car accident in California, is sued personally in California court, loses the lawsuit, and is ordered to pay a judgment of $1 million to the California plaintiff? Now, the question of outside liability comes into play.

In addition to attempting to seize all of Cory’s personal assets, the plaintiff can also try to seize Cory’s 100% membership interest in his California LLC. California law, unlike Nevada, does not restrict the ability of a plaintiff to foreclose on Cory’s membership interests in the LLC. This means a judge applying California law could rule that the creditor can take over Cory’s interest in his LLC. While this is a drastic remedy, it can and has been done in California, in which case, the creditor can access the assets within the LLC.

What if Cory had created a Nevada LLC? Under Nevada law, foreclosing the interest of an LLC member is not permitted, and a creditor may only obtain what is called a “charging order.” A charging order is basically a lien over any economic interest, whereby the creditor waits in line essentially until there is a liquidation or distribution event of the member’s interest in the LLC. A holder of a charging order cannot force a distribution though, and cannot participate in any management of the LLC, or the investments of any of its assets. Thus, if Cory as the manager of the LLC does not provide for a distribution to himself as a member, his creditor does not receive anything from the LLC. Nevada – unlike California – does not provide for any other “equitable remedies” available to a creditor, including reverse veil piercing, constructive trusts, resulting trusts, or alter ego theories, which would allow for a judge to reach into the LLC and disburse assets to the creditor.

While it may seem that a Nevada LLC is far superior to a California LLC when it comes to outside liability (and it is), the real question is which state law would a California judge apply to an accident that occurs in California, where the victim was a Californiai resident, where the defendant was a California resident, and in which the property owned by the LLC is located in California? It stands to reason that a California judge may be hard pressed to apply any law other than California to those facts, in which case, some practitioners will opine that it does not matter if you use a California LLC or a Nevada LLC if the nucleus of operative facts is based in California only.

The flip side of this coin is based on practical realities. For example, if Cory had created a California LLC, there is no debate that California law would apply. The only question will be whether the judge offers the creditor equitable remedies, foreclosure, or a charging order. However, if Cory had created a Nevada LLC, wouldn’t Cory’s legal team have more arguments to make in defending that action? Wouldn’t there be just a bit more uncertainty as to how the case will develop, which choice of law the judge will ultimately decide to use, as well as which remedies will be granted? The fact that there is greater uncertainty means that any settlement discussion will favor Cory and his legal team more so than if Cory had not created a Nevada LLC.

A savvy owner will recognize these facts for what they truly mean. The LLC per se, on its own, cannot prevent you from getting sued and does not automatically make lawsuits disappear. The purpose of an LLC is to limit liability, hence its full name: a limited liability company.

It should be noted that some clients believe that a Wyoming LLC is superior in that Wyoming LLCs offer greater anonymity protections. This is true in that members of Wyoming LLCs are afforded greater privacy protections than owners of LLCs in other states. But this is just one factor that must be taken into consideration when selecting under which state law to incorporate. Furthermore, the Corporate Transparency Act was passed by Congress as part of the Anti-Money Laundering Act of 2020. This legislation will soon require disclosure of beneficial ownership interests in all entities, including LLCs.

2. Who Should Own the LLC?

Another major question to resolve is who should an LLC. As noted earlier, I will discuss the use of irrevocable trusts in this section, so knowing a bit about the basics of an irrevocable trust will be helpful.

Unrelated to the question of asset protection, an LLC should be treated like any other asset in that it is subject to probate at death. As a result, individuals should never own LLCs in their own names, otherwise, the LLC will need to be probated in order for ownership to pass to their next of kin.

Whether you or your living trust is the owner of the LLC means a big difference when it comes to probate, but when it comes to asset protection, neither forms of ownership provide any protection from lawsuits.

Many clients believe or have read that it’s far better to have LLCs owned by other LLCs. The typical structure involves members owning only one LLC holding company, which in turn owns the membership interests of additional operating LLCs. From a matter of ease and governance, this structure offers some benefits. For instance, instead of assigning ownership of each LLC to your living trust, you may need to just assign the ownership of your holding company to your trust. But if the holding company is owned by you or your living trust, or even if it is a series LLC, ultimately the outside liability analysis discussed above does not change much. That is to say, the creditor can seek to attach ownership in your holding LLC, which in turn, owns your operating LLCs.

Therefore, in my opinion, the best way to own an LLC is not through your own name or living trust, but rather through an irrevocable trust, because – unless it is a domestic asset protection trust (DAPT) – you will not be the beneficiary of your irrevocable trust. Therefore, a creditor has nowhere to turn if they are trying to enforce a judgment against you, because neither you nor your living trust owns your LLC; instead, your irrevocable trust owns the LLC, and you are not a beneficiary of your irrevocable trust. Thus, there are a variety of different kinds of irrevocable trusts that can own an LLC: gifting/inheritance trusts (set up for the exclusive benefit of your children or grandchildren for example), DAPTs (set up for the benefit of the LLC member), SLATs (typically set up for the benefit of spouses and children), and hybrid-DAPTs (in which the LLC member is not named as a beneficiary of the trust but can be added in later if needed).

In general, multi-member LLCs offer greater asset protection than single-member LLCs. One of the reasons for this is with single member LLCs, there is a greater likelihood that creditors would be able to foreclose on the interests of the member (rather than be given a charging order) since there is no risk of infringing on the interests of other LLC members when there is only one member.

Let’s go through an example of the power of irrevocable trusts owning LLCs.

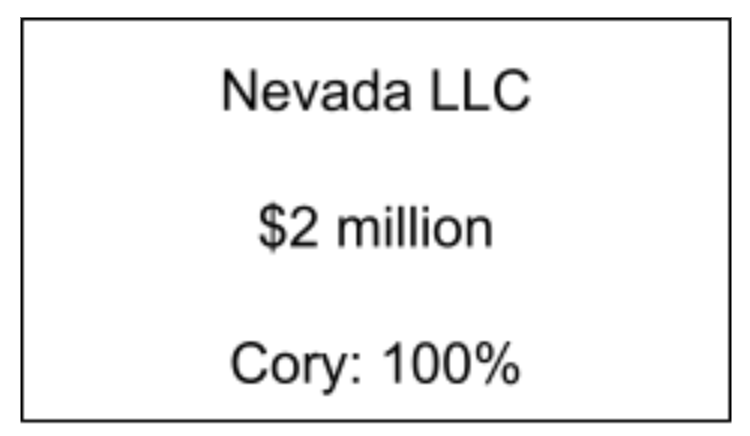

Let’s imagine Cory creates a Nevada LLC to own his California rental property. Let’s also imagine that in creating the LLC, Cory owns it in his living trust. If there is outside liability, and if the creditor obtains only a charging order (Nevada affords creditors the exclusive remedy of a charging order), Cory’s assets are protected until or unless Cory authorizes for a distribution of the assets to himself. While this generally is a good result for Cory, and shifts settlement discussion in his favor, how does Cory actually get money out of the LLC if he needs it? If he attempts to take distributions out through salary, management fees, or loans, the judgment creditor can seize these amounts depending on how the charging order is worded. Thus, even with a Nevada LLC with charging order protection, this is still the problem when it comes to the practical realities of disbursing money out of the LLC. The problem with charging orders is sometimes the client themselves are essentially locked out of their own LLC.

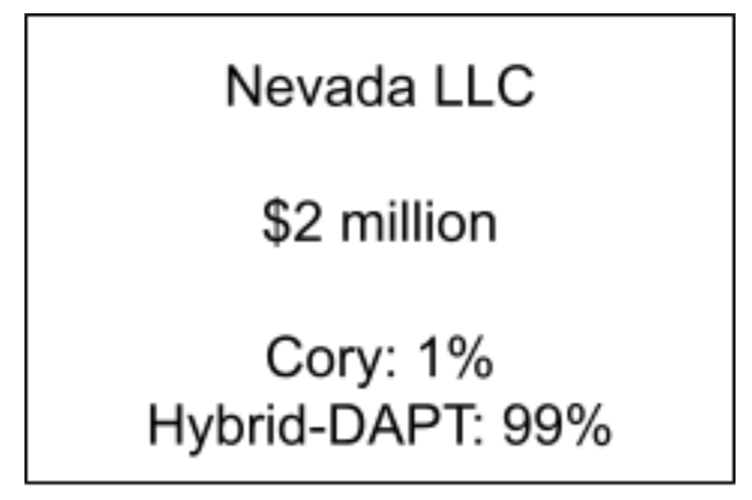

But what if Cory instead owned the LLC as follows: 1% in his name and 99% by his Nevada hybrid-DAPT? What would happen then?

Here, with a charging order granted to Cory’s judgment creditor, Cory can still pull out distributions without worrying about the judgment creditor since distributions will flow out of the Nevada LLC in the same proportions. For example, 99% of the disbursements will be distributed not to Cory, but to his hybrid-DAPT, where he is not listed as a beneficiary. Thus, the creditor cannot prevent this distribution or access it. Instead, the creditor can only seize 1% of the distributions that are made out to Cory himself. If the beneficiaries of the hybrid-DAPT are Cory’s family members, then Cory can indirectly benefit from the distributions made to the hybrid-DAPT.

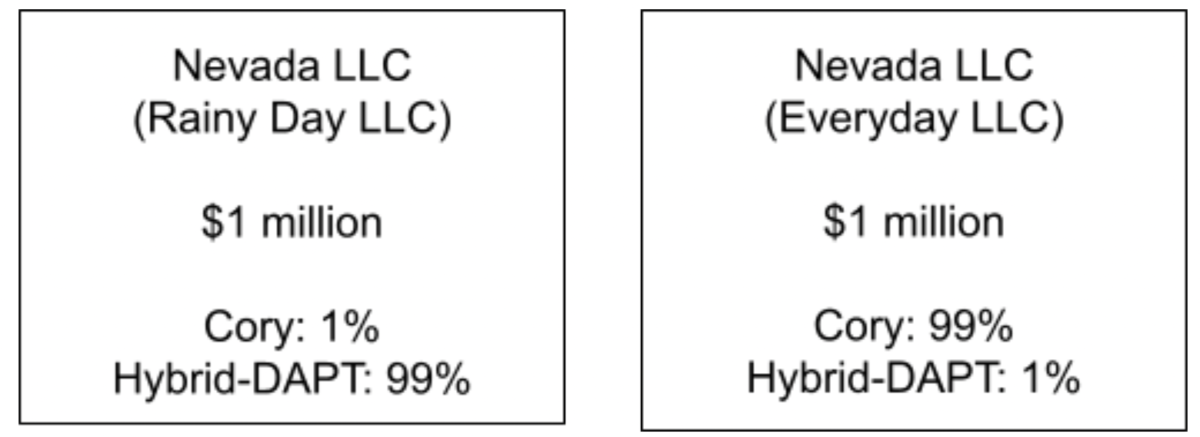

In fact, using two Nevada LLCs instead of one leverages the situation even more. For example, imagine Cory put $1 million in one Nevada LLC that was owned 1% by him and 99% by his hybrid-DAPT (Rainy Day LLC), and put $1 million in another Nevada LLC that was owned 1% by his hybrid-DAPT and 99% by him (Everyday LLC).

In this situation, the Everyday LLC is the one Cory routinely uses to take distributions from, since he will be getting 99% of the distributions. But in the event of a judgment creditor who was granted a charging order, the Everyday LLC will stop giving distributions and instead Cory will choose to take distributions from the Rainy Day LLC, whereby he (and thus his creditor) will only receive 1% of any distributions and the hybrid-DAPT (and not the creditor) will receive 99% of the distributions. Using these two LLCs will give Cory the flexibility of maximizing distributions at all times.

Depending on the circumstances, rather than the LLC being owned by a hybrid-DAPT, the LLC will be owned by one or more different irrevocable trusts. For example, for California real property, it very common to setup family LLCs in which a minority of the LLC (less than 50%) is owned by generation 1 (the parents or their living trusts), while the majority of the LLC (more than 50%) is owned by generation 2 (the descendants) or gifting trusts established for their benefit. We do this not only because of asset protection but also to avoid property tax reassessment in California at death. In fact, LLCs in California are governed by Proposition 13 instead of Proposition 19, which means that at death of a parent, reassessments can be avoided by using LLCs.

Keep the Right Perspective

It is wholly unreasonable to believe that LLCs prevent lawsuits altogether or immunize someone entirely. Instead, the LLC is a planning tool that offers incredible and powerful benefits, not only from the standpoint of minimizing taxes but also promoting greater asset protection. But, like anything, LLCs must be compliant with state law. If not, LLCs – like corporations – can be pierced through and your personal assets can be taken.

It is important to become educated with the various principles at play in order to determine what is the correct way to structure your LLC. While multiple member LLCs are superior to single member LLCs, this makes the need to draft a robust, thorough Operating Agreement even greater. While a Nevada LLC may be superior to a California LLC from an outside liability perspective, from an inside liability standpoint, they make no difference. And finally, it is always better if the LLC is owned by someone other than you, whenever possible, and if so, using irrevocable trusts offers a great deal of protection.

But these strategies must be weighed against the increased setup costs, annual fees, greater administrative burdens (e.g., filing annual tax returns, complying with state rules), and the real-life realities of refinancing, lender approvals, and the seeming loss of flexibility and control.